Pennsylvania-based EQT Corporation (EQT) is the largest natural gas producer in the United States, focused on the exploration and production of gas in the Appalachian Basin, particularly the Marcellus and Utica shales. As an upstream energy company, it generates revenue by extracting and selling natural gas, making its performance closely tied to commodity price movements. The company is currently valued at a market cap of $37 billion.

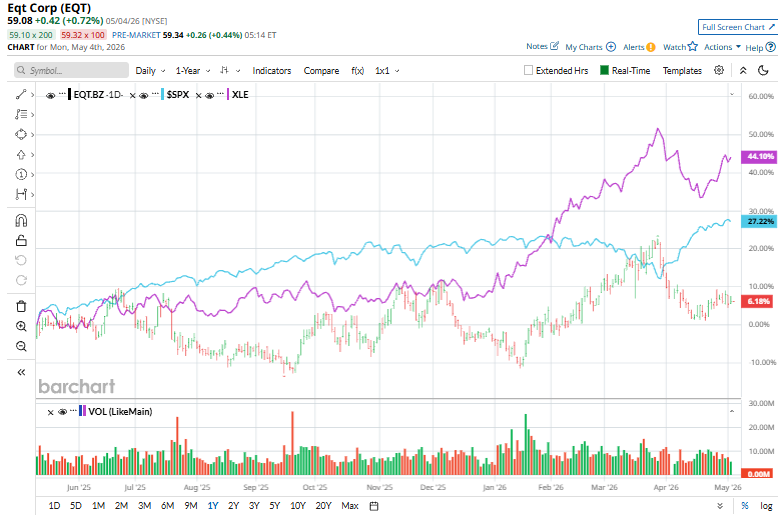

The energy giant has underperformed the broader market over the past year. EQT stock prices have soared 13.9% over the past 52 weeks, lagging behind the S&P 500 Index’s ($SPX) 26.6% gains. However, in 2026, the stock has surged 10.2%, outpacing the $SPX’s 5.2% rally.

Narrowing the focus, EQT has trailed the sector-focused State Street Energy Select Sector SPDR Fund’s (XLE) 44.9% gains over the past 52 weeks and 32.8% rise on a YTD basis.

On Apr. 21, EQT released its FY2026 Q1 earnings and its shares popped 3.1% in the next trading session. Total sales volume reached 618 Bcfe, exceeding guidance, while realized natural gas prices improved to around $5.08/Mcfe, supporting a sharp increase in revenue to roughly $3.13 billion. Adjusted EPS climbed 97.5% year over year to $2.33, and adjusted EBITDA jumped 50.4% to $2.68 billion.

For FY2026, which ends in December, analysts expect EQT to deliver an adjusted EPS of $4.58, up 50.2% year-over-year. Furthermore, the company has a solid track record of earnings surprises. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

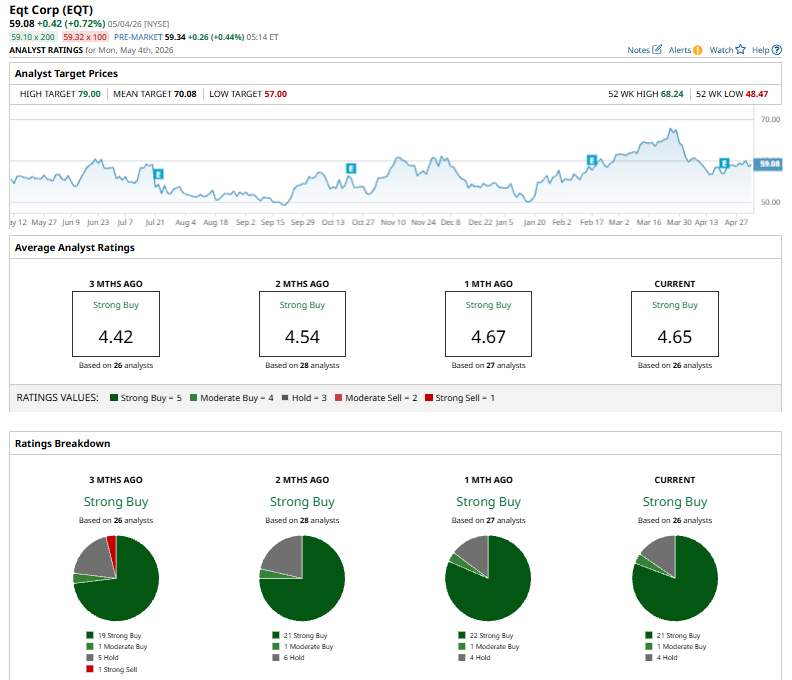

Among the 26 analysts covering the EQT stock, the consensus rating is a “Strong Buy.” That’s based on 21 “Strong Buys,” one “Moderate Buy,” and four “Holds.”

The configuration is bearish than a month ago when the stock had 22 “Strong Buy” suggestions.

On Apr. 24, UBS analyst Josh Silverstein slightly lowered the price target on EQT to $74 from $75 while maintaining a “Buy” rating on the stock.

EQT’s mean price target of $70.08 suggests a 18.6% upside potential. Meanwhile, the Street-high target of $79 represents a notable 33.7% premium to current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Micron Technology Huge, Unusual Put Option Activity - a Bullish Signal as MU Rises 12%

- As Wall Street Eyes $2,000 for SNDK Stock, Sandisk Is Counting on New Business Models (NBMs) to Drive Growth

- Little-Known Baldwin Stock Just Jumped into the Spotlight on an Anthropic Deal

- NXP Semiconductors Stock Nears All-Time High. Here's Why NXPI is a Buy Now.