Since December 2024, Stryker has been in a holding pattern, posting a small return of 1.1% while floating around $376.76.

Is now the time to buy SYK? Or does the price properly account for its business quality and fundamentals? Find out in our full research report, it’s free.

Why Do Investors Watch SYK Stock?

With over 150 million patients impacted annually through its innovative healthcare technologies, Stryker (NYSE:SYK) develops and manufactures advanced medical devices and equipment across orthopedics, surgical tools, neurotechnology, and patient care solutions.

Three Positive Attributes:

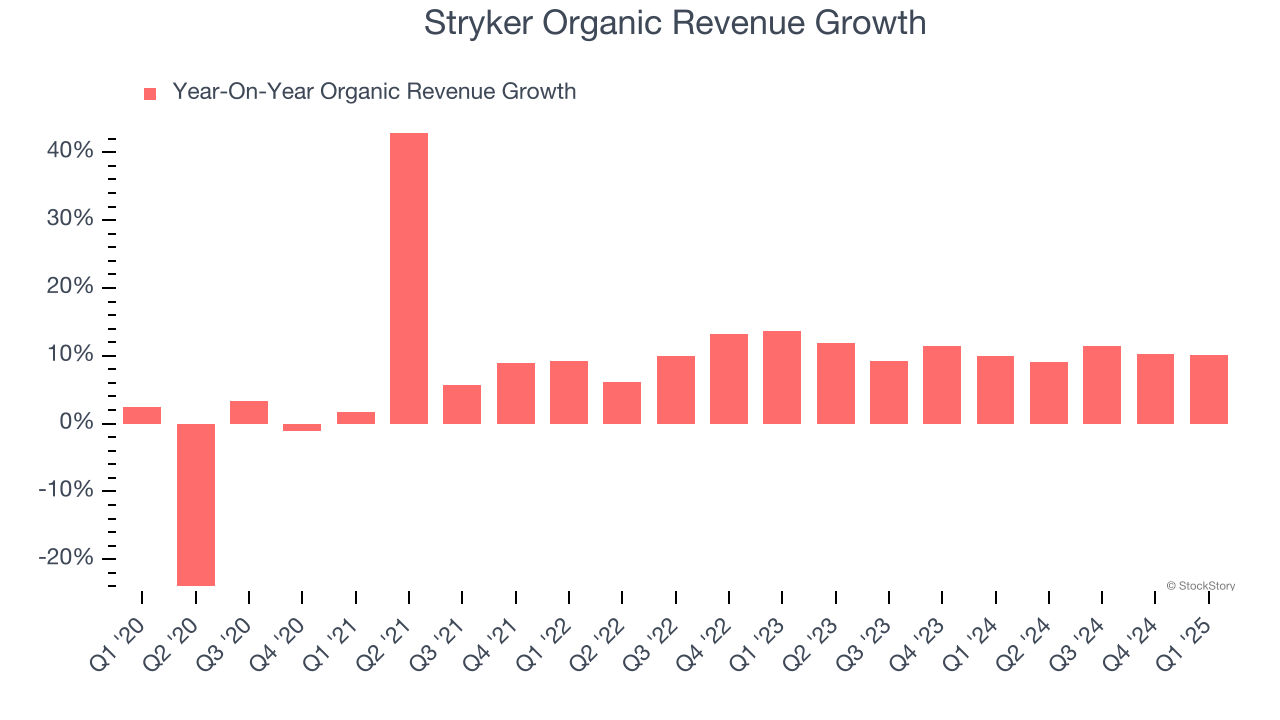

1. Organic Growth Indicates Solid Core Business

We can better understand Medical Devices & Supplies - Diversified companies by analyzing their organic revenue. This metric gives visibility into Stryker’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Stryker’s organic revenue averaged 10.4% year-on-year growth. This performance was solid and shows it can expand steadily without relying on expensive (and risky) acquisitions.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $23.22 billion in revenue over the past 12 months, Stryker sports economies of scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

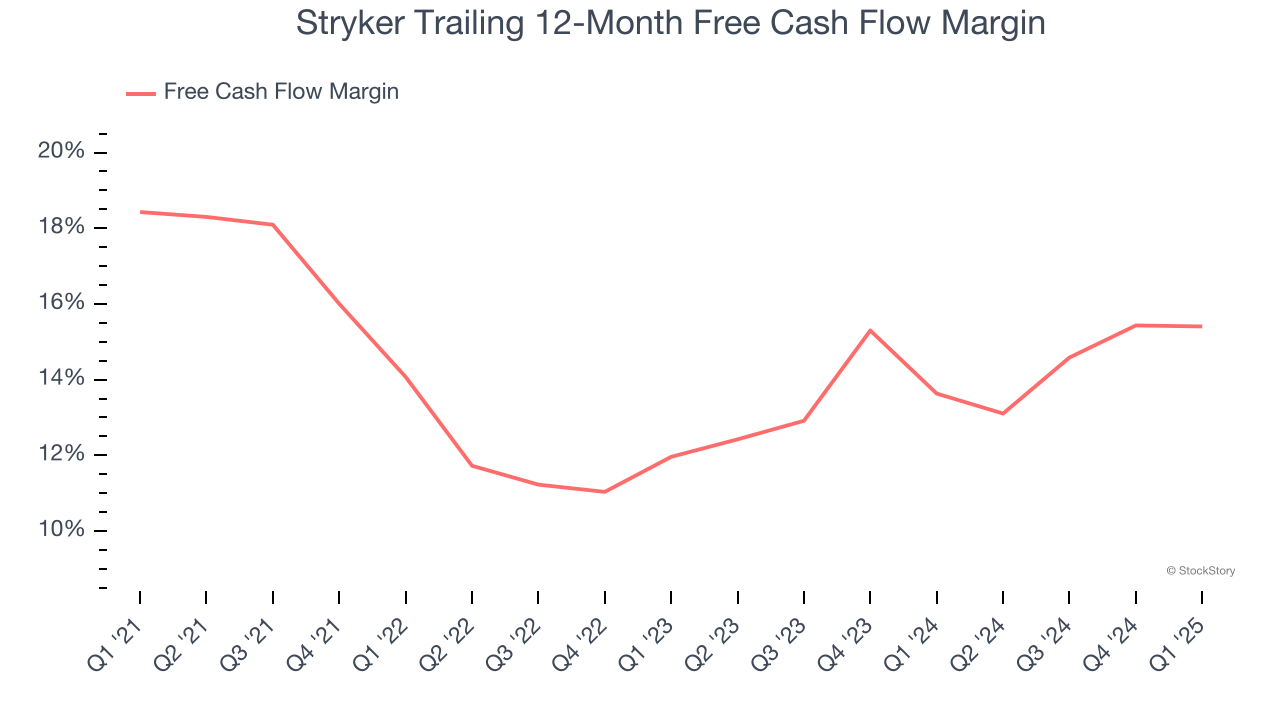

3. Impressive Free Cash Flow Margin Opens Growth Opportunities

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Stryker has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14.6% over the last five years, better than the broader healthcare sector.

Final Judgment

There are definitely things to like about Stryker, but at $376.76 per share (or 27.3× forward P/E), is now the right time to buy the stock? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Stryker

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.